Then & Now

May 3, 2022

The current environment illustrates how quickly market conditions can change. In many ways, present conditions are the polar opposite of what we witnessed for much of the last two years. Not long ago, the Nasdaq 100® Index, which is home to many former high flyers, was plowing into new highs. Fast forward to today, the index is down 21.1% year-to-date (YTD) and just declined 13.3% in the month of April alone…its worst month since 2008. Even more remarkable, the top 5 stocks in the S&P 500® Index lost $1.3 trillion of their value in April.

Warren Buffett recently noted the market had become a “gambling parlor” where stocks were treated like “poker chips.” Indeed, over the last year we witnessed rampant speculation and aggressive risk taking. Meme stocks, SPACs, unprofitable growth companies and bitcoin were all the rage this time last year. We expressed caution about such mania. As we wrote in our Q1 2021 letter:

“In addition to unwanted inflation, persistent economic stimulus can also fuel risky speculation. As noted in our intra-quarter update, there has been evidence of speculative froth in corners of the market such as chat room stocks (e.g. the GameStop frenzy), SPACs (special purpose acquisition companies), bitcoin and high-growth “story stocks.” In select cases, “price” and “value” seem to have become disconnected.”

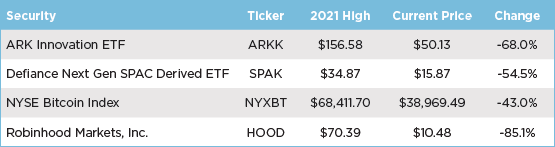

My how things have changed. Consider the following examples. The popular ARK Innovation ETF (ARKK) peaked at $156.58 in 2021. It is now trading at $50.13. SPAK, an ETF that holds shares of SPACs was $34.87. It is now $15.87. Bitcoin was valued at $68,411.70. It is now $38,969.49. And shares of Robinhood (HOOD), one of the very enablers of the stock casino, were trading at $70.39. The stock is now $10.48/share.

5/2/2022

A year ago, we were cautious about chasing risk. We remain somewhat cautious about the overall market given the double whammy of slowing earnings growth and declining P/E multiples alongside tighter monetary policy. However, it’s hard not to acknowledge that some fluff has come out of the market and the overall risk/reward profile looks more balanced. Even more “conservative” stocks are down sharply as market weakness has spread. We aren’t firmly embracing risk, but it could make sense to start incrementally taking on more risk as prices decline. At a minimum, it is important to fight the natural tendency to become increasingly negative as markets decline. Even if stocks aren’t “cheap” yet, they are cheaper than they were.

The speculative fervor of last year is done and we generally aren’t interested in many of the lower quality names that have blown up. But, a number of high quality and durable franchises have also been pummeled during the recent melee. Admittedly, many of these were formerly trading at lofty and unsustainable valuations.

Fast forward to present, we have very recently been incrementally taking on a little risk at much more attractive prices. We recognize we could be early, but timing bottoms in various names will be virtually impossible. Taking baby steps towards risk could prove prudent over the course of the next few years – even if it looks foolish in coming months.

Again, equity markets face headwinds that make recent declines somewhat unsurprising and we aren’t changing our tune with regards to expecting more subdued returns than prior years (the start to 2022 has gone a long way to subduing returns already!). However, we can definitively say that these and other high-quality stocks should have much less downside than before. We are not calling this an “all in” moment. Perhaps we are just a little less cautious given a somewhat improved risk/reward setup for the market.

Important Disclosures: Past performance is not indicative of future results. Diversification and asset allocation does not ensure a profit or guarantee protection against a loss. There is no guarantee that a company will continue to pay dividends. The statements and opinions expressed in this article are those of Davenport Asset Management as of the date of the article, are subject to rapid change as economic and market conditions dictate, and do not necessarily represent the views of Davenport & Company LLC. This article does not constitute investment advice, is not predictive of future performance, and should not be construed as an offer to sell or a solicitation to buy any security or make an offer where otherwise unlawful. Investing in securities carries risk including the possible loss of principal. Individual circumstances vary.

Important Definitions: The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. Standard & Poor’s Financial Services LLC, a division of S&P Global, is the source and owner of the registered trademarks related to the S&P 500 Index. The Nasdaq 100 Index is a basket of the 100 largest, most actively traded U.S companies listed on the Nasdaq stock exchange.